Friends, here it is! I’ve written a book entitled Teach a Kid to Save: A Fun, Hands-on Approach to Building Smart Money Habits. Itnow has a cover design and is available for pre-order at Amazon, Barnes & Noble, Baker Publishing Group, or wherever you like to buy books. Go ahead and order one. It will ship on January 13.

Why isn’t it available before Christmas? My editor patiently explained to me that “people don’t buy self-help books for Christmas. They’re a New Year thing.” That makes sense. So if you are planning on panicking that you broke the bank Christmas shopping and want get a strong start next year, this is the book for you.

Or rather, for your kids, since they’re the main ones who are to benefit from the book.

Speaking of breaking the bank for your kids, there is a new survey showing that parents are struggling with debt. A reporter (Jana Pollack) for Parents.com reached out to ask me about the study and why parent debt is growing. Here’s what she wrote (click here for the full article):

National Debt Relief and Talker Research looked at financial pressures facing 2,000 US parents of kids ages 0-18. Their findings show that 6 in 10 American parents have gone into debt for their children. Of those, 81% prioritize paying for their kids over paying their debt, and nearly half say that their debt is unmanageable...

According to Dr. Stephen Day [of the Center for Economic Education] at Virginia Commonwealth University and author of "Teach a Kid to Save,” rising interest rates are one of the primary contributing factors to a rise in debt among parents.

“In the wake of COVID, we had a surge in inflation; and to combat inflation, the Fed raised interest rates,” he explained. “To the extent that people were already using debt, [for example] credit cards, that made the interest rates for those worse, and people just were not able to budget...”

In other words, many people planned to finance purchases with a certain amount of debt—but then all of a sudden found themselves with skyrocketing costs they hadn’t planned for.

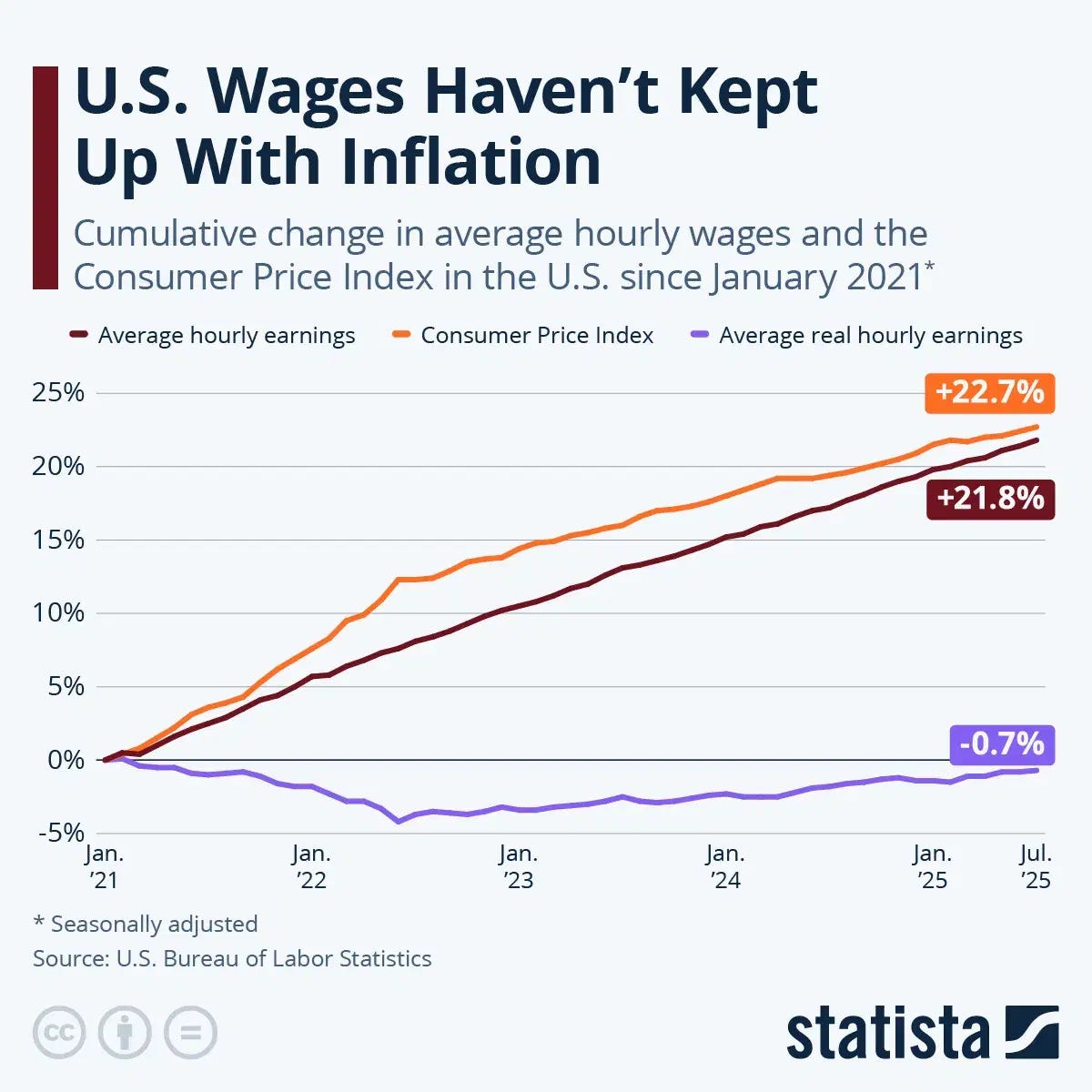

Another factor is wages, which have not kept up with inflation. “Wages lag behind rising costs, and people fill the gap with debt—which suddenly has a much higher interest rate,” Dr. Day added.

The blue line shows the approximate difference between wages and inflation, that is, people’s earnings (why it’s not exact, I don’t know). Notice that real earnings were falling in 2021-2022, and have been playing catch-up since.

The culture of parenting has changed drastically, too. It’s not just costs that have risen—expectations for parenting have also ballooned in recent years. More engaged parents combined with social media platforms that connect kids to trends that incite comparisons, embarrassment, and peer pressure if they don’t conform, has created an environment where some parents may feel as though they are actually required to spend any amount of money necessary to see their kids excel both socially and academically.

“If you look at the cultural shift in the past couple of decades, we just parent more intensively,” said Dr. Day, who cites that change as another factor which increases parents’ debt. Parents are paying for more sports team fees, more extra curricular activities, and any other extras that they think might boost their child’s development.

Studies back up that claim, and acknowledge that parenting today is harder than it was twenty years ago. Studies also confirm that social media creates added pressure to parent in a way that can sometimes feel competitive with those in your orbit (and beyond, with many parents seeing people they don't know on social media sharing their ideal parenting strategies).

What I’m saying is that I think that parents are in debt for much the same reason that everyone else is. Wages have lagged a bit behind inflation for the past five years. To combat inflation, the Federal Reserve raised interest rates, sort of like how firefighters spray water on a burning house. The water stops the fire, but it still soaks and ruins your stuff.

When interest rates go up, debt is suddenly more expensive. Debt brings risk. It adds uncertainty to the future. We think that we have plans to pay it off, but if something unexpected happens – like a surge in interest rates – we’re in for a nasty surprise.

On the other hand, if you’ve saved up money, then higher interest rates help you. You get a better return on your savings. That’s why it’s best to give your monthly payments to yourself in the form of savings, then to a bank in the form of interest payments. Buying with saved money not only gets you a higher standard of living in the long run, but it also decreases interest rate risk.

You can help your kids save by buying my book! Yes, I will remind you in future editions of Paper Robots. But now is as good a time as any to click that Amazon link (Or B&N or Baker, etc.) and pre-order. Then you can snuggle up with it on January 13 and make plans for the new year. Thank you!

Congrats! I love the book cover. Well done!